The IRS provides answers to some key questions about coronavirus-related distributions from IRAs, 401(k)s and other eligible retirement plans; and expands qualification for it, by association.

On March 27, 2020 the Coronavirus Aid, Relief, and Economic Security (CARES) Act was signed into law, in response to the coronavirus disease 2019 (COVID-19) outbreak and its impact on the economy, public health, state and local governments, individuals, and businesses. Section 2202 of the CARES Act permits qualified individuals to take coronavirus-related distributions, from eligible retirement plans, which are penalty free and qualify for other special tax benefits. But there were- and still are- many unanswered questions about coronavirus-related distributions. The Internal Revenue Service (IRS)- in their quest to answer these questions, have provided guidance, including the recently issued Notice 2020-50 which provides some unexpected answers and opportunities. This article covers five of these.

What’s The Big Deal About Coronavirus-Related Distributions?

Coronavirus-related distributions are a hot commodity right now, as they allow qualified individuals to access funds from their tax deferred retirement savings accounts without the usual immediate tax consequences and penalties. These are:

- Exemption from the 10% early distribution penalty: A 10% early distribution penalty applies to distributions taken before the account owner reaches age 59 ½, unless the amount qualifies for an exception. For a SIMPLE IRA, the penalty is increased to 25% if the distribution is made from a SIMPLE IRA that has not been funded with a SIMPLE IRA contribution for at least two years. Coronavirus-related distributions have been added to the list of exceptions.

- Three years to include in income: A distribution from a retirement account is generally included in income for the year in which the amount is distributed. A coronavirus-related distribution is an exception to this general rule, allowing the account owner to include the amount in income ratably over three years, starting with 2020. If the account owner prefers, an election can be made to include the entire amount in income for 2020.

- Three years to roll over: An account owner who wants to exclude a distribution from income by returning it to an eligible retirement account- where it would continue to benefit from tax deferred growth, may do so by rolling over the amount within 60 days of receipt. This 60-day period is waived or extended under limited circumstances, one of which is a distribution that qualifies as a coronavirus-related distribution. Under this waiver, a coronavirus-related distribution that is eligible for rollover, can be rolled over within 3 years of receipt.

These tax friendly features make a coronavirus-related distribution- which is capped at $100,000 per person- an attractive solution for those who are facing financial difficulties. But, one requirement for eligibility is that they are available only to qualified individuals. The following are some of the surprising revelations provided by the IRS in Notice 2020-50, including the expanded definition of a ‘qualified individual’ for coronavirus-related distribution purposes.

1. You Can Get Qualified Through Your Spouse; Or The Butcher, The Baker, Or The Candlestick Maker- If They Share Your Principal Residence

A coronavirus-related distribution must meet three key requirements. It must be made:

- At any time from January 1, 2020 through to December 31, 2020,

- From an eligible retirement plan, and

- By a qualified individual.

For this purpose, an eligible retirement plan means:

- An individual retirement account (IRA),

- An individual retirement annuity (IRA) other than an endowment contract,

- A qualified plan, such as a pension, 401(k) or profit-sharing plan,

- A 403(a) annuity plan,

- A governmental and eligible deferred compensation 457(b) plan, and

- A 403(b) account or annuity.

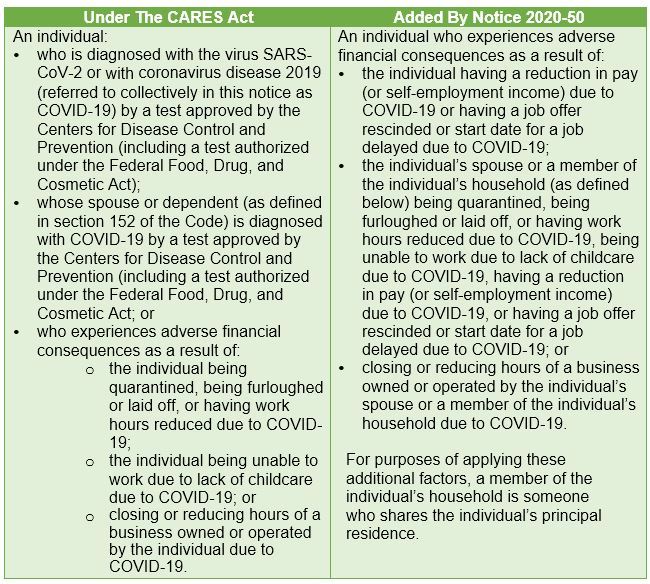

The definition of a qualified individual has been expanded under Notice 2020-50 to include your spouse or a member of your household, who faces adverse financial consequences as a result of COVID-19. The following is the definition under the CARES Act and the addition provided under Notice 2020-50:

This expanded definition now confirms that if you are not adversely affected by COVID-19- financially speaking- you would still be eligible for a coronavirus-related distribution if your spouse or a member of your household experiences adverse financial consequences as a result of COVID-19.

1. You Can Take It Even If You Don’t Need It

Jimmy Cliff’s very popular song “You Can Get It If You Really Want” is appropriate here. Because, if you are a qualified individual, you may take a coronavirus-related distribution if you want to, even if you do not have a financial need arising from COVID-19.

As to whether you should, is a different question of course, and one that should be seriously discussed with a financial and/or tax advisor.

2. A Distribution From A Beneficiary Account Can Be A Coronavirus-Related Distribution

One of the outstanding questions about who is a qualified individual, for purposes of taking a coronavirus-related distribution, is whether the holder of a beneficiary account under an employer sponsored retirement plan or IRA could qualify. IRS Notice 2020-50 confirms any distribution received by a qualified individual can be treated as a coronavirus-related distribution, even if the distribution is made from a beneficiary IRA or beneficiary account under an employer sponsored retirement plan. As a result, the income from such amounts are eligible to be spread ratably over 3-years.

3. The Only Beneficiary Permitted To Roll Over A Coronavirus-Related Distribution Is A Spouse BeneficiaryThe tax code and all official guidance make it clear that only a spouse beneficiary may roll over a distribution taken from an inherited retirement account. Notice 2020-50 also confirms that even if the distribution is a coronavirus-related distribution, it is not eligible for tax-free rollover treatment if it is made to a beneficiary, unless the beneficiary is the surviving spouse of the deceased account owner.

4. A Distribution That Is Ineligible For Rollover Cannot Qualify As A Coronavirus-Related Distribution

Amounts distributed from eligible retirement plans can be restored to the same or another eligible retirement plan through rollovers- where permitted, only if the amount is eligible to be rolled over. If an amount is not ordinarily eligible to be rolled over, such an amount is not eligible for the benefits available to coronavirus-related distributions. These amounts include certain substantially equal periodic payments, and a distribution that is made on account of hardship of an employee.

An exception applies to a hardship distribution, if it meets the requirements to be considered a coronavirus-related distribution. Under that exception, the usual hardship withdrawal rules are disregarded, and the coronavirus-related distribution rules would apply- making the amount eligible for rollover.

Notice 2020-50 confirmed that because there is no required minimum distribution (RMD) for 2020, any distribution that would have otherwise been an RMD except for the CARES Act, is an eligible rollover distribution- and eligible for the coronavirus-related distribution benefits, if taken by a qualified individual. This RMD exception does not apply to RMDs from defined benefit plans- as those are not waived, and distributions taken by beneficiaries from retirement accounts- unless the beneficiary is the surviving spouse of the decedent.

Because You Can, Does Not Mean That You Should

A large number of Americans face adverse financial consequences as a result of the COVID-19 pandemic- including loss of job-related income. And for many, a coronavirus-related distribution is the only solution to staying above choppy financial waters. But, if you are a qualified individual who does not need to take a coronavirus-related distribution, it might be in your best financial interest to leave the amount in your retirement savings account.

There are factors that must be considered- most of which are not broached in this article. Regardless of your choice, be sure to consult with your financial and tax advisor before taking action.